Visa and mastercard settle new swipe-fee deal

Visa and mastercard swipe fees will change after nearly 20 years of legal disputes. The settlement aims to lower credit card processing fees for U.S. merchants. Moreover, it gives stores more control over which cards they accept. Consequently, these changes may affect how consumers use premium cards or rewards cards. Shoppers might not notice immediate effects, but over time, the settlement could reshape payment methods and influence consumer spending habits. The agreement follows years of legal pressure and complaints about high credit card fees. In addition, merchants may save money on transactions, which could indirectly benefit shoppers.

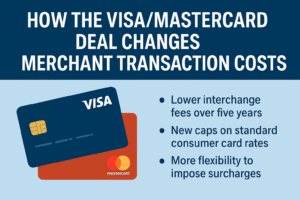

How the deal between visa and mastercard will alter merchant transaction costs

The settlement reduces interchange (swipe) fees from 2–2.5% by 0.1 percentage points over five years. Standard consumer card rates will be capped at 1.25% for eight years. This gives stores predictable costs. Merchants can now add surcharges to certain card payments. This helps cover processing costs or encourages the use of lower-fee cards. VISA says the deal provides real relief. Mastercard notes that smaller stores will benefit from simpler rules and lower fees.

Regulatory pressure and the legal backdrop

After 20 years of disputes, VISA and MASTERCARD reached a settlement. Merchants had complained about inflated swipe fees. A previous $30 billion settlement was rejected by U.S. District Judge Margo Brodie. She believed it did not help merchants enough. The new agreement removes the “honor all cards” rule. Stores can now refuse certain cards, like premium or rewards cards. A $21 million merchant education program is included. It helps stores understand payment costs. Some groups, including NACS, remain critical of the deal.

Implications for consumers and the future of visa and mastercard payments

Shoppers may see lower prices or extra fees. How stores use the new flexibility will matter. Some may add fees for high-cost cards. This could affect premium and rewards card usage. Mastercard says the settlement benefits both businesses and consumers. Smaller stores may save money and improve service or prices. Critics warn these benefits might not last. High-fee reward cards remain an issue. VISA and Mastercard could still change card types or network fees.

Potential impact in Canada

Although the settlement mainly affects the U.S., it could impact Canada. Canadian merchants often watch U.S. payment decisions closely. Many use the same Visa and Mastercard networks. Reduced fees or more flexibility for U.S. stores may encourage similar changes in Canada. This may also affect how Canadians use premium and rewards cards. Payment choices at stores across the country could shift. Canadian consumers might see adjustments in card usage patterns.

Overall impact

The VISA and MASTERCARD settlement may reshape payments in the U.S. Swipe fees are slightly lower. Card rules are simpler. Merchant education is funded. The deal still needs court approval. Its success depends on how stores apply the new rules. Some may add fees or refuse certain cards. Shoppers may not see immediate effects. Over time, card usage could change, especially for rewards cards. Small merchants benefit most. Large stores see limited gains. The settlement marks a major shift after 20 years of litigation.